Thinking about buying a home with a VA loan in 2026? Getting pre-approved is a really important first step. It basically tells you how much you can borrow and shows sellers you’re serious. We’ll walk through what VA home loan pre approval means and how to get it done.

What is a VA Home Loan Pre-Approval?

Getting pre-approved for a VA home loan is getting a tentative “yes” from a lender at the outset of shopping seriously for homes. It’s a step in which a lender closely examines your finances, your service history, and your credit to see how much they would be willing to lend you. This is not a final loan approval, but it’s an important indicator of what you can afford.

Just like you wouldn’t go grocery shopping without confirming your wallet, right? Pre-approval does the same thing for home shopping. It provides a realistic price range so you’re not wasting your time viewing homes that are well out of your budget.

And when you find a place you like, the pre-approval letter makes your offer look that much stronger to sellers. Many sellers in the current market won’t even look at an offer without one of these letters attached.

Here’s a quick rundown of what lenders check during this phase:

- Your Service History: They’ll look at your Certificate of Eligibility (COE) to confirm you meet the VA’s service requirements.

- Your Credit Score: While the VA doesn’t set a minimum score, lenders usually have their own guidelines they follow.

- Your Income and Employment: They need to see that you have a stable income to handle monthly mortgage payments. This usually involves looking at pay stubs, W-2s, and bank statements.

This initial review helps both you and the lender understand your borrowing power and identify any potential hurdles early on. It sets the stage for a smoother process down the line.

Why is VA Home Loan Pre-Approval Crucial?

The first step to take is getting pre-approved for a VA loan. Its not a quick estimation, but rather a deep examination of your finances by a lender. This gives you a clear idea of how much you can reasonably get, which is very useful when you’re actually starting to shop around for houses.

Understanding Your Budget

To determine your actual budget, you’ll need pre-approval. When lenders decide how much they’re willing to lend, they take into account your income, debts, and credit history. So you won’t be wasting your time looking at homes that are more than you can afford.

It also makes it easier to determine what your monthly payments will be like, including principal, interest, taxes, and insurance. Knowing this in advance puts a much sharper focus on house-hunting.

Use our VA loan affordability calculator alongside your pre-approval to get a full picture of what your monthly payments will look like, including principal, interest, taxes, and insurance.

Strengthening Your Offer

A pre-approval letter shows the seller that you’re serious about making an offer on a house and are financially able to do so. In competitive markets, sellers tend to favor offers from pre-approved buyers because that means a deal is more likely to close without the financing falling apart.

It means you have done your homework and are a strong candidate. This can help your edge over other buyers who have not been preapproved yet. In fact, a strong pre-approval letter is one of the most essential aspects of the VA loan process itself.

Navigating the Market with Confidence

With pre-approval, you can shop for a home with far greater confidence. You do know your borrowing limit and have a good idea of what you can afford. This means you can spend more time focusing on finding the right home and less time worrying whether they’ll approve you for a loan.

It also helps to guide your real estate agent, who will know what price range to target. It makes the entire process of home buying feel less complicated and daunting.

When you get pre-approved, a lender reviews your income, assets, and credit history. This is a detailed review, moreso than pre-qualification, and provides a more precise estimate of the loan amount you would qualify for. It’s an important step before seriously looking for a house.

Here’s a quick look at what pre-approval helps clarify:

- Your maximum loan amount: This sets your home-buying budget.

- Potential monthly payments: Understanding costs beyond the sticker price.

- Areas for financial improvement: Identifying any issues that need addressing before final approval.

- Seller confidence: Demonstrating you’re a qualified buyer.

Eligibility Requirements for VA Loan Pre-Approval

So, you’re considering utilizing your VA home loan benefit? That’s great! But before you can imagine sipping cocktails on the porch of your new digs, there’s some stuff you’ll need to figure out. Pre-approval for a VA loan is not just a matter of form, but ensure that you meet the basic prerequisites. This means examining your service record, your credit, and your income.

Service Requirements

For starters, you have to show that you served. That’s what the VA loan program is all about, after all. The Department of Veterans Affairs has clear rules about how long and under what circumstances you need to have served to be eligible. Typically, this entails a specific number of days on active duty or a particular length of time in the National Guard or Reserves.

The Certificate of Eligibility (COE) is the official document that indicates you qualify for these service requirements. Your lender will procure this for you, and it’s an important piece of the pie when it comes to getting a VA loan approved.

Credit Score Considerations

The VA does not impose a minimum credit score, but lenders generally do. They assess your credit history to estimate the chance that you will repay the loan. The higher your credit score, the smoother the pre-approval process will go, and the better loan terms you’re likely to receive.

Generally, lenders are looking for scores in the mid 600s or above, but this can change. It may be worth checking your credit report beforehand to understand where you stand. If your score isn’t where you want it to be, there are things you can do before applying to improve it.

Income and Employment Verification

Lenders want to see that you have a steady income and employment. They’ll want to see a track record of steady work, typically over at least the past two years, and often with the same employer or in the same type of job. This allows them to assess whether you can easily afford your monthly mortgage payments.

You’ll generally need to submit recent pay stubs, W-2s, and perhaps tax returns. If you’re self-employed or have other sources of income, you should be ready to supply more documentation. This verification is an important component in the preparation for VA loan underwriting.

If you have a VA loan on the horizon, understanding these requirements is the first step toward successfully sailing through the process. It’s not simply about serving; it’s about showing you can financially handle service. Lenders want to see a track record of attractive financial management, so they closely examine income, employment, and credit history. This extensive check reassures you and the lender that the loan is secure.

Here’s a quick rundown of what lenders typically look for:

- Service Verification: Proof of eligible military service (your COE).

- Credit History: A history of responsible debt management.

- Income Stability: Consistent employment and sufficient income to cover payments.

- Debt-to-Income Ratio: How your monthly debt payments compare to your gross monthly income.

Meeting these requirements for VA loan pre-approval is your ticket to exploring homes with confidence. It shows sellers you’re a serious buyer and helps you understand your purchasing power, making the house hunt much more productive.

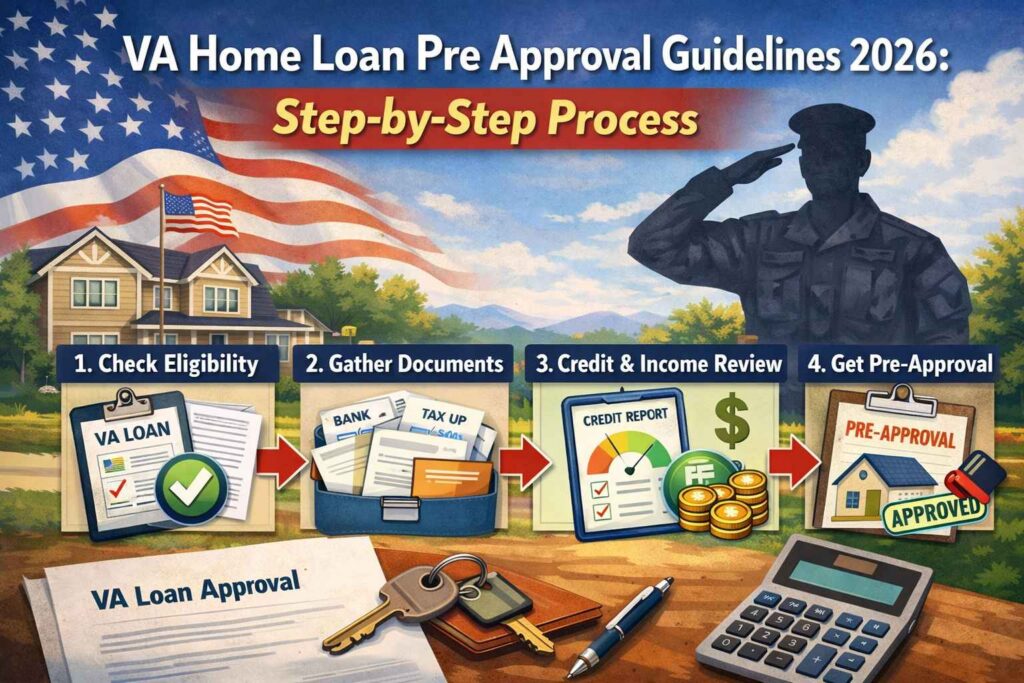

The Step-by-Step VA Home Loan Pre-Approval Process

VA home loan preapproval is a relatively simple process, but it requires several important steps. Consider it as preparing the land before building your dream house. It’s not just about having the letter, it’s about ensuring you are prepared for the home-buying process. This is a major element of any first-time VA home buyer guide.

Gathering Necessary Documentation

Long before you ever speak to a lender, you will want to get your paperwork together. This allows the whole process to flow more easily. To obtain your Certificate of Eligibility (COE), you’ll show proof of your military service. This document is extremely important because it proves your entitlement to the VA loan benefit.

Lenders will want to see other proof of income, such as pay stubs and tax returns. They’ll also want to look at your credit history.” Having these documents prepared allows you to act more swiftly when you discover the right house.

Here’s a quick rundown of what to gather:

- Certificate of Eligibility (COE): This confirms your service and entitlement.

- Proof of Income: Recent pay stubs, W-2s, or tax returns.

- Bank Statements: To show available funds for closing costs and reserves.

- Identification: Driver’s license or other government-issued ID.

The pre-approval process is designed to give both you and the lender a clear picture of what you can afford. It’s about setting realistic expectations from the start.

Applying with a VA-Approved Lender

After you’ve got your documents, it’s time to search for a lender who has experience with VA loans. Not all lenders are created equal, so look for one that specializes in VA mortgages, they’ll understand the nuances of your entitlement, COE, and service documentation far better than a general mortgage lender.

If you’re planning to build rather than buy, you’ll also want to line up a VA approved builder at this stage, since the VA requires that all new construction be completed by a builder registered and approved through their program.

You want a pre-approval letter stating the maximum amount you can borrow. This is the letter you will use to show sellers that you are serious about purchasing. It’s an essential part of the VA mortgage application steps. Consider VA loan options to get started.

Once you receive your pre-approval letter, you can start house hunting in confidence because you know your budget. Note, however, that pre-approval is a good sign, but the actual loan approval occurs after you find a home and your lender completes their thorough underwriting process, including the VA appraisal.

Wrapping It Up

So, that’s the lowdown on getting pre-approved for a VA loan in 2026. It might seem like a lot of steps, and yeah, there’s paperwork involved, but honestly, it’s pretty straightforward when you break it down. Getting that pre-approval letter really sets you up for success, showing sellers you’re serious and giving you a solid idea of what you can afford.

Just remember to talk to your lender, have your documents ready, and don’t be afraid to ask questions. It’s a big benefit, and taking the time to do it right makes all the difference in getting into your new home.

Frequently Asked Questions

What’s the main difference between pre-qualification and pre-approval for a VA loan?

Consider pre-qualification an educated “guess” about how much you’ll probably be able to borrow, based on what you tell the lender. Pre-approval is more serious; the lender will conduct a review of your credit and finances so they can give you a concrete number that they’re willing to lend. It would be kind of like receiving a ‘maybe’ instead of a ‘yes, within this amount.

Do I need a Certificate of Eligibility (COE) before getting pre-approved?

You can begin the pre-approval process without it, but your lender will absolutely need your COE to close on your VA loan. It’s evidence that you are eligible for the VA home loan benefit. This can be done quickly, so it’s a good idea to inquire about it early on with many lenders.

How long does the VA loan pre-approval process usually take?

It varies, but being preapproved tends to come relatively quickly, a few hours or a day or two at most, if you have all your documents in hand. It could also be as quick as the information you provide, and how busy the lender is.

What kind of documents will I need for a VA loan pre-approval?

You’ll probably want documentation of your military service (such as a DD-214), recent pay stubs, W-2s from the past two years, and bank statements. If you get disability pay, you’ll need those award letters as well. Essentially, anything that demonstrates your income, assets, and service history.

Can my credit score affect my VA loan pre-approval?

Yes, which means that while VA loans do not have a set minimum credit score by the VA itself, lenders often will. They use your credit score to gauge how reliably you’ve repaid debt in the past. Generally speaking, the higher your score, the easier it is to be approved for a loan, and you may qualify for better terms.

What happens after I get my VA loan pre-approval letter?

Once you have your pre-approval letter, it tells you how much you are likely to be able to borrow, which helps narrow your house hunt. You can then partner with a real estate agent to discover a home that fits your budget. Once you have the right place to call home and an accepted offer, you’ll go on to start the full loan application steps as well as the underwriting process.