Thinking about buying a home in Alabama in 2026? It’s a big step, and figuring out the mortgage situation can feel a bit overwhelming. You’ve probably heard that interest rates go up and down, and that can really change how much house you can afford.

This guide is here to break down what you need to know about mortgage rates in Alabama, so you can feel more prepared when you start looking for your dream home.

Understanding Alabama Mortgage Rates

If you’re in the market for a home in Alabama, it’s important to know about mortgage rates. It is these rates, sometimes referred to as the Alabama home loan interest rates, that can have a significant impact on the amount of your monthly payment. It’s not just a number that will impact the overall cost of your home over many years. There are a number of factors that determine your actual rate.

| Metric | Figure |

|---|---|

| Median home price in Alabama | $248,000 |

| Average days on market | 52 days |

| Year-over-year price change | +4.2% |

| Alabama homeownership rate | 70.1% (national avg: 65.8%) |

| Monthly mortgage payment at 6.42% | ~$1,320/month |

Consider your credit score; the better the score, the better the rate. Lenders also consider your earnings, the amount of debt you currently have, and the amount of money you intend to invest in a down payment. The health of the Alabama housing market as a whole is also a factor. Rates could rise slightly if there is a lot of home-buying activity because lenders will have more business.

Factors Influencing Mortgage Rates in Alabama

Several factors can impact mortgage rates in Alabama. So, what drives the rates of the housing market in Alabama? First, the macroeconomic context is important. Interest rates can be affected by events in the world and in the country. The Fed’s actions on short-term borrowing rates can also have a ripple effect in the mortgage market. Beyond that, your personal financial situation is key.

| Credit Score Range | Est. Rate | Monthly Payment ($250K) | 30-Year Total Interest |

|---|---|---|---|

| 760–850 Best | 6.10% | ~$1,519 | ~$296,840 |

| 700–759 | 6.35% | ~$1,556 | ~$310,160 |

| 680–699 | 6.65% | ~$1,604 | ~$327,440 |

| 660–679 | 6.90% | ~$1,645 | ~$342,200 |

| 640–659 | 7.40% | ~$1,730 | ~$372,800 |

Your credit history is a big part of it; a 680 score is good, but it may not qualify you for the lowest rates. Lenders are looking for a consistent income and a manageable debt-to-income ratio. Another factor is the size of your down payment. The more you can put down, the lower the interest rate will be, since the lender will have less risk.

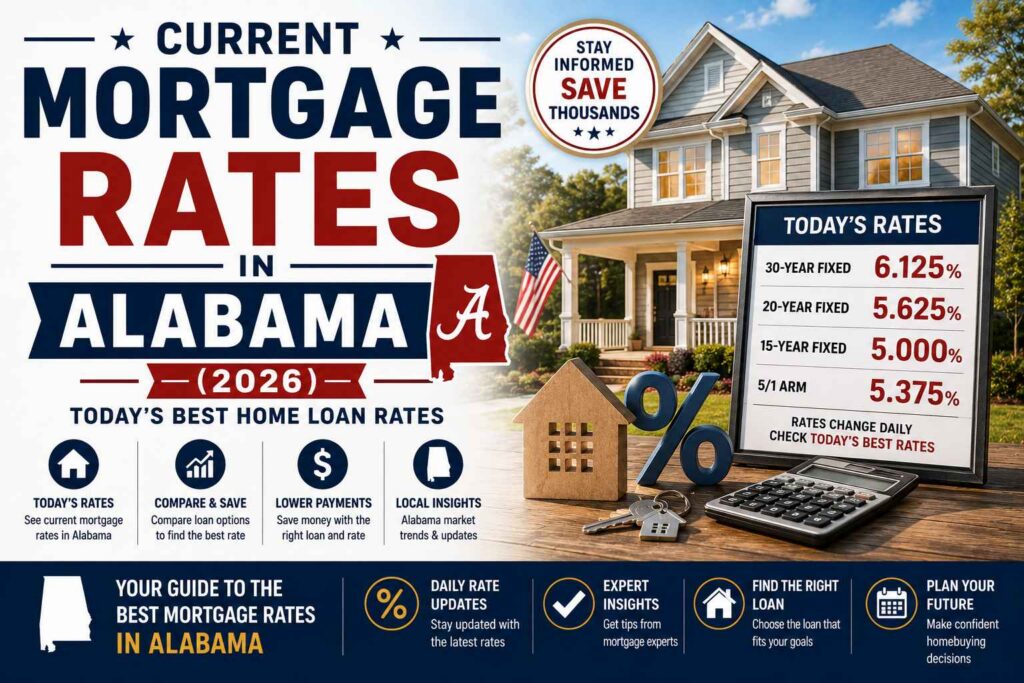

Current Mortgage Rate Trends in Alabama

Alabama mortgage rates are on the rise. It’s useful to be aware of the latest rate trends, but keep in mind that rates may fluctuate from day to day and even hour to hour.. They are affected by economic indicators and market activities.

It’s useful to be aware of the latest rate trends, but keep in mind that rates may fluctuate from day to day and even hour to hour.

When it’s time to purchase, it’s easy to try to time the market, but it’s best to concentrate on locating a rate that fits your budget. Trying to time the market can lead to a missed opportunity to buy a great home.

Keep in mind that advertised rates may be samples. They’re based on specific borrower profiles and might not reflect what you’ll be offered. Always obtain individual quotes to find out what your individual rate and payment would be.

Here’s a general idea of what influences the average mortgage cost in Alabama:

- Credit Score: Higher scores generally get lower rates.

- Down Payment: A larger down payment can reduce your rate.

- Loan Term: Shorter loan terms often have lower rates.

- Economic Conditions: National and global economic health play a role.

- Federal Reserve Policy: Actions by the central bank impact rates.

| Loan Type | Average Rate | Monthly Payment (per $250K) |

|---|---|---|

| 30-Year Fixed | 6.42% | ~$1,567 |

| 15-Year Fixed | 5.85% | ~$2,094 |

| 5/1 ARM | 6.53% | ~$1,584 |

| FHA 30-Year | 6.10% | ~$1,519 |

| VA 30-Year Best Rate | 5.90% | ~$1,484 |

When you’re looking at Alabama refinance rates, the same factors generally apply. It’s always a good idea to compare offers from different lenders to find the best deal for your situation.

Types of Mortgages Available in Alabama

If you’re interested in purchasing a home in Alabama, you’ll discover that there are a number of different types of mortgages available. It is not a one-size-fits-all, which is good as everyone’s financial situation is different. Let’s take a look at the primary choices you’re likely to encounter.

| Loan Type | Min Down Payment | Min Credit Score | PMI Required | Best For |

|---|---|---|---|---|

| Conventional | 3–20% | 620+ | Yes (under 20%) | Strong credit buyers |

| FHA | 3.5% | 580+ | Yes | Lower credit buyers |

| VA 0% Down | 0% | No minimum* | No | Veterans & military |

| USDA | 0% | 640+ | No | Rural Alabama buyers |

| ARM (5/1) | 5–20% | 620+ | Varies | Short-term owners |

Fixed-Rate Mortgages

This is likely to be the most prevalent kind of home loan. With a fixed-rate mortgage, the interest rate you get at the beginning stays the same for the entire life of the loan. So, if you get a 30-year loan at 5% interest, then you will pay 5% interest for the entire 30 years.

This will help you to plan your budget better because you know what you are going to have to pay every month. You’ll be able to see exactly how much your principal and interest payment will be each month, which makes it easier for you to plan your finances in the long run.

Adjustable-Rate Mortgages (ARMs)

ARMs are a little different. Typically, they offer a lower interest rate for a period of time, such as five or seven years, before the rate increases. The interest rate then may fluctuate on a periodic basis, typically every 6 months or 1 year. These changes are linked to a financial index, such as the Secured Overnight Financing Rate (SOFR).

This will result in a change in your monthly payment amount. ARMs may be a good choice if you’ll sell the home or refinance before the end of the initial fixed period, or if you don’t mind the prospect of switching payments. Most ARMs have caps that cap the amount the rate can rise at each adjustment and throughout the life of the loan, providing some protection.

FHA Loans and VA Loans in Alabama

Loans that are available to certain individuals. The Federal Housing Administration (FHA) backs FHA loans, which are ideal for borrowers with low credit scores or limited down payment savings. These typically have a lower down payment than traditional loans.

Qualified veterans, active military service members, and surviving spouses are eligible to apply for a VA loan. The loans are backed by the Department of Veterans Affairs and can offer some amazing benefits, such as no down payment required for many borrowers.

If you are a veteran or currently serving in the military, definitely consider VA loans in Alabama, they can be a great financial decision. The decision of the type of mortgage one should get is a significant one. It will impact your monthly budget and total interest you will pay over the years. Try to learn the differences and determine which one suits your financial objectives and your tolerance of the possibility of payment adjustments.

How to Find the Best Mortgage Rates in Alabama

If you’re ready to purchase a home in Alabama, you want to be certain that you’re getting the best deal on your mortgage. That’s smart! When it comes to finding the best mortgage deal that Alabama has to offer, it’s not simply about the first lender that you visit. This will require a little bit of work, but it can save you a significant amount of money over the course of your loan.

Shopping Around for Lenders

This is likely the most crucial step. Never take your local bank or the bank recommended by your real estate agent without comparing other banks. Rates and fees vary from lender to lender and may not be optimal for everyone.

It’s important to get quotes from at least three lenders. This will help you understand the variety of options and may even provide some leverage in your negotiations.

Here’s a simple way to approach it:

- Know Your Budget: Before you even talk to lenders, figure out exactly how much house you can realistically afford. This means looking at your income, savings, and monthly expenses.

- Get Pre-Approved: Apply for pre-approval from a few lenders. This gives you a solid idea of how much you can borrow and what your interest rate might look like. It also shows sellers you’re serious.

- Compare Loan Estimates: Once you have pre-approvals, lenders will send you a Loan Estimate. This document breaks down all the costs associated with the loan. Look closely at the interest rate, APR (which includes fees), and any points you might be paying. Make sure you’re comparing apples to apples.

Remember that advertised rates are often just samples. To get your actual rate, you’ll need to provide details about your credit score, down payment, and the property’s location. Don’t be afraid to ask lenders to explain anything you don’t understand on the Loan Estimate.

Improving Your Credit Score

The rate that you’re offered on your mortgage is a major consideration with regard to your credit score. The higher the score, the lower the interest rate, and the more money you can save.. If your score isn’t where you’d like it to be, work on your score prior to applying for a mortgage.

It’s important to pay bills on time and to keep credit card balances low. Any improvement can help you in getting the best mortgage deals Alabama lenders offer. A credit score of 750 is very good and can lead to better rates, for instance. It is important to have consistent and responsible financial habits to continue to enhance them and reap even more financial rewards.

Understanding Closing Costs

In addition to the interest rate, there are closing costs. These are charges that you pay when you close your mortgage. These can consist of appraisal charges, title insurance, origination charges, and much more.

Some lenders may offer a slightly lower rate but charge higher closing costs; always compare the APR, not just the interest rate, to get the true picture.

It’s important to understand the total cost of the loan, not just the interest rate. Make sure lenders explain all closing costs so you can make a fair comparison. Another way to get the best mortgage deals in Alabama is by shopping around.

Alabama Mortgage Rate Forecast for 2026

Forecasting mortgage rates for an entire year is a challenge, and let’s face it, no one has a crystal ball. But if we examine current trends and economic indicators, we can have a general idea of what we can expect in Alabama for 2026.

At this time, rates are fluctuating a bit in May 2026. The 30-year fixed-rate mortgage has fallen slightly in recent days, but remains above last year’s levels. There are many factors, including economic news from around the world, Federal Reserve policy decisions, and the overall health of the housing market. It’s a balancing act, as mortgage-backed securities purchases by government agencies have helped rates not go too high when the economy had other news to suggest they should.

It’s crucial to keep in mind that mortgage rates are estimated, not guaranteed. It’s possible to miss out on a great home when trying to time the market right. Don’t get bogged down in the number; just concentrate on what you can do.

Here’s what to keep in mind for 2026:

- Economic Influences: Keep an eye on inflation data and labor market reports. These will likely continue to be major drivers of interest rate movements.

- Federal Reserve Actions: Any changes in the Fed’s short-term borrowing rates can impact longer-term loan costs, including mortgages.

- Housing Market Activity: A busy housing market might mean less competition among lenders to offer the lowest rates.

When you’re thinking about purchasing a home in AL next year, you can use our mortgage calculators to get a general idea of how much you’ll be paying in monthly payments for various scenarios of interest rates. Even if the actual rates aren’t decided, this tool can be very useful for budgeting. Keep in mind that advertised rates are not necessarily the actual rates you will receive; it’s best to contact lenders directly for custom quotes.

It’s easy to see why people want to wait for rates to hit historic lows that they’ve experienced in previous years, but that’s not likely to happen again for a while. There are a number of complex factors that affect the market, and it’s best to think about finding a home that suits your requirements and budget at this time, and knowing what the market rates are at the time.

Wrapping It Up

Keep in mind that these are averages and your rate will vary based on your individual circumstances, such as your credit score and the amount of down payment you make. Shopping around and comparing offers from different lenders is really worthwhile. A slight variation on the interest rate can mean significant savings over the term of the loan. Watch these trends but don’t wait too long to purchase if you’ve discovered the proper residence.

Frequently Asked Questions

What are mortgage rates in Alabama right now?

As of May 18, 2026, the average rate for a 30-year fixed mortgage in Alabama is around 6.42%. For a 15-year fixed mortgage, it’s about 5.85%, and for a 5-year adjustable-rate mortgage, it’s approximately 6.53%. Keep in mind these rates can change daily.

What factors affect mortgage rates in Alabama?

Several things can influence mortgage rates. These include the overall health of the economy, decisions made by the Federal Reserve, and how active the housing market is. Even global events can play a role.

What’s the difference between a fixed-rate and an adjustable-rate mortgage?

With a fixed-rate mortgage, your interest rate stays the same for the entire time you have the loan, making your monthly payments predictable. An adjustable-rate mortgage (ARM) starts with a set rate for a few years, but then the rate can go up or down based on market changes, meaning your monthly payment could change.

How can I get the best mortgage rate in Alabama?

To find the best rate, it’s a good idea to compare offers from several different lenders. Also, improving your credit score and understanding all the costs involved, like closing costs, can help you secure a better deal.

Will mortgage rates go down in 2026?

Predicting exact future rates is tricky. While rates can move up and down, it’s unlikely they’ll return to the very low rates seen in 2020-2021 anytime soon. It’s best to focus on finding the right home and a rate that works for your budget now, rather than trying to perfectly time the market.

What is APR, and why is it important?

APR stands for Annual Percentage Rate. It’s more than just the interest rate; it includes other costs and fees associated with the loan, like closing costs and mortgage insurance. Because it shows the total cost of borrowing, APR gives you a clearer picture of what your mortgage will really cost you.